Strategic Roth Conversions

History shows that tax rates are volatile

The recently enacted Tax Cuts and Jobs Act slashed individual tax rates, accordingly Roth conversions just went on sale but the tax bargain may not last forever.

What is a Roth conversion and why would a taxpayer do one?

The primary advantage of converting a traditional IRA to a Roth IRA is the funds will not be subject to income tax upon withdrawal if certain rules are followed.

Keep in mind that Roth contributions are not the same as a Roth conversion. Roth contributions have income limits and Roth conversions do not. Also, a Roth conversion is part science and part art.

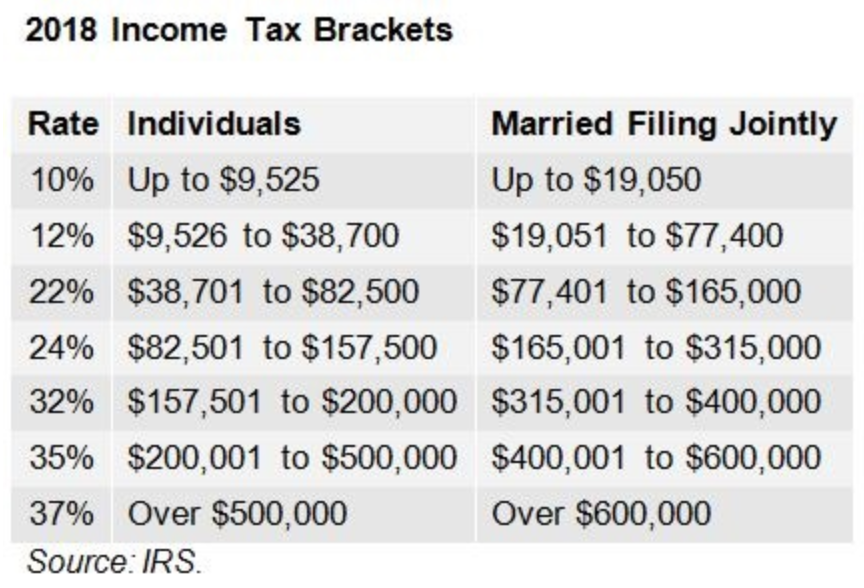

Here are some parameters: First, let’s look at the federal tax brackets. Almost everyone’s tax bracket came down in 2018. Many married folks that were in the 33% tax bracket in 2017 will find themselves in the 24% bracket, a 27% reduction. For example, if a married couple was contemplating a Roth conversion and their 2018 projected taxable income is $285,000, then the most they should consider converting would be $30,000. At that amount, it would keep this couple in their current tax bracket.

You may have an aversion to paying taxes. However, there are ways to minimize the bite that taxes take. For instance, the taxpayer may consider pairing the Roth conversion with increased charitable contributions or medical expenses. Or, the taxpayer may have experienced a business loss, which can be used to offset the Roth conversion income.

Some Roth conversions can be tax-free. Here is a real life example: When Dean married his wife, Julie, she had only a 401(k) account but no existing traditional IRA. Due to income limits, Julie could not make a Roth contribution. Currently, Julie has an existing traditional IRA that for 364 days a year sits with a zero balance. But this January, Julie made a nondeductible contribution of $6,500 into her traditional IRA. Then in early February, she converted her traditional IRA ($6,500) to a Roth and the tax cost was zero!

That example was pretty easy to follow, but now I’m going to add a little complexity so stay with me here. What if Julie had made pretax contributions to her IRA in earlier tax years?

Roth IRA conversion pro-rata rule

Some taxpayers mistakenly believe that they can get around the income tax liability created as a result of making a Roth IRA conversion by rolling over only the portion of their IRA plans that were made with nondeductible contributions.

For example: If Julie had $20,000 in a traditional IRA account, which includes $3,500 in investment earnings, $10,000 in tax-deductible contributions, and $6,500 in nondeductible contributions, Julie may reason that she can avoid creating an income tax liability by rolling over the $6,500 from the nondeductible contributions.

Unfortunately, the above strategy is not going to fly with the tax authorities. Roth conversions are done pro rata, which holds that the tax-exempt portion of your rollover contribution must constitute only a pro-rata share of the total rollover.

There are ways around the pro-rata rule, for example, if the pretax money came from a defined contribution plan, then Julie could ask her current employer to accept the pretax monies since they originally came from a qualified plan. Maybe the pretax funds are small so picking up some taxable income in one year won’t be too taxing—especially now with lower tax rates!

Therefore, when contemplating a Roth conversion, some taxpayers will be better candidates then others. We just need to determine the best opportunities.

As long as you have the money set aside to pay the taxes due and the tax rate is thought to be lower than the future tax rate then this may be a good opportunity to do a Roth conversion.

Also, keep in mind, that the taxpayer does not have to do a full conversion, she can do a partial Roth conversion and take a number of years to complete a full conversion. Just keep in mind that we currently have low tax rates and we don’t know if and/or when the tax rates may change.

One point to keep in mind, and this is new for 2018 conversions and beyond, is that a Roth conversion is not reversible (i.e. can not be recharacterized).

Roth IRAs have other tax benefits

Take note of the following:

- No required minimum distributions (RMDs) at age 70½ for the IRA owner during their lifetime.

- Access to tax- and penalty-free withdrawals* to help manage the income tax bill in retirement.

- An individual can continue to fund a Roth IRA even after 70½ as long as the person has earned income, subject to income limitations.

- Probably the best legacy asset you can leave a loved one, if one inherits a Roth IRA because the RMDs are required but the beneficiaries may be able to use their own life expectancy. Also, it will be tax-free and the Roth assets will continue to grow tax-free.

- Roth IRAs can be set up for minors who have earned income of their own. Parents could gift the cash to their children to fund the Roth provided that the contribution to the Roth IRA is not more than the minor’s earned income in that year. It’s better to fund a Roth rather than a traditional IRA when the tax rate is low.

*Penalty-free withdrawals may be subject to certain conditions. Please check with your tax professional prior to taking a withdrawal.

Information provided by SEI Investments Management Corporation (SIMC), a wholly owned subsidiary of SEI Investments Company (SEI).

SIMC and SEI are not affiliated with Digital Wealth, LLC.

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice. This information is for educational purposes only.

Digital Wealth, LLC does not provide tax advice. Please note that (i) any discussion of U.S. tax matters contained in this communication cannot be used by you for the purpose of avoiding tax penalties; (ii) this communication was written to support the promotion or marketing of the matters addressed herein; and (iii) you should seek advice based on your particular circumstances from an independent tax advisor.